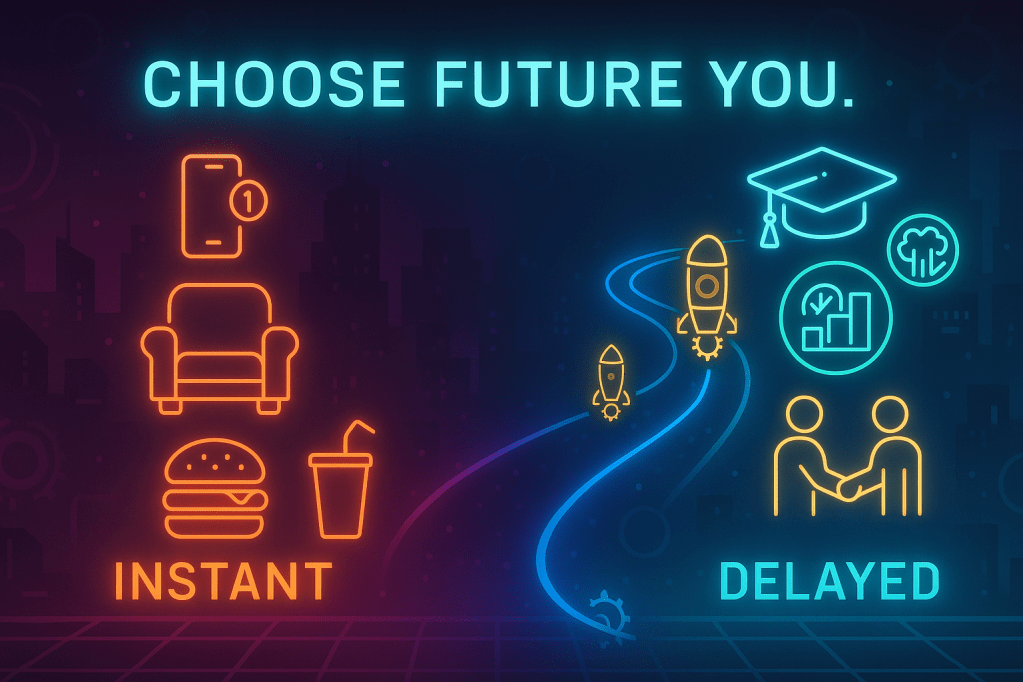

How Delayed Gratification Helps You

By Eva M.A.

When you think of money you always think, “I want to spend my money for this or that.” Sometimes you can spend it however you want, but you should not always spend money to satisfy your wants. You should save up most of your money for your actual needs, like rent, gas, groceries, utilities. You might ask yourself, “How do I stop wanting to spend my money and not have that impulsiveness of wanting something I don’t need?” Well, delayed gratification will be the skill you need to stop all the impulsive wanting to buy.

How does delayed gratification work? Delayed gratification: If you understand that it is a difficult concept, it will become easier. There are two parts of the brain, the part that makes you impulsively buy and then there is the prefrontal cortex that is responsible for planning, reasoning and long term thinking. In MBA Financial Strategist it shows that in delayed gratification the prefrontal cortex overrides the limbic system that wants you to get things that you shouldn’t. Delayed gratification practice is just self control and having the ability to not impulsively spend $1,000 right now, when later you can have $1,050, if you save up right.

There is this marshmallow experiment that showed that you can find a way to not want to impulsively buy things you shouldn’t. The marshmallow experiment consisted of scientists putting a marshmallow on a table and telling a kid that they can eat it, or, if they wait at least 15 minutes they can have two marshmallows. In the experiment, there were kids that ate it right away and some that did wait for the bigger award later. There was follow up research that showed that the children who waited for the bigger reward did better in their studies, maintained healthier relationships, and had better finance skills as adults. Though, in later studies, a different scientist shows that the marshmallow experiment does not reliably predict the financial aspect as you move on as an adult, but it shows the impulsiveness you can have and the ability to wait for the long-term goal and get a better outcome.

Impatience is something that always gets us impulsive and wanting something we do not need, like snacks. How can we help that and why does it happen? We like to get things based on our emotions and not look at the future. We don’t want to look at the bigger picture because the future is unknown, but, if you envision something that is good you can get that impulse to stop. You can make the future look good, like being financially stable and having the money to get things that are important later, like getting a house or car you really want. Thinking ahead and envisioning the future as good would make you want to stop being impulsive to get short-term wants. Another crucial aspect is education on finances. It is important to know how you can budget and not be in debt, and to know how to control emotions and look at the bigger picture. This helps you achieve the goal of not impulsively buying things you do not need.

Thinking ahead and envisioning the future as good would make you want to stop being impulsive to get short-term wants.

My uncle Javier Jesus Ruiz Gomez is great at financial aspects of life. He shared to me a time he gave up short-term reward for a bigger long-term goal. He told me that in law school he had times that he would spend with family and friends, but there were times he would turn down plans because law school was demanding. He traded that short-term award to a long-term goal, because he knew that staying focused and using all those long hours of studying would give him the long-term goal he wanted. He saw that waiting would pay off later, and having the ability to wait would give him the chance to build a successful career and would be worth the short-term sacrifice. A big part of prioritizing future success over immediate comfort that he showed me, was always keeping your future goals in mind, which could be financial stability, career growth, or building a secure future. Having all those things in mind, he said, helped with the short term comfort he wanted sometimes. Be creative about finding affordable ways to enjoy life. He said, “I don’t believe prioritizing the future means never having fun. It just means being intentional and responsible about decisions, so that today’s choices support tomorrow’s goals, instead of working against them.”

There are many strategies you can use to help you in delayed gratification. You can set clear financial goals that will be a reminder to you and will help you not impulsively give you the urge to spend impulsively. Visualizing long-term impact will help a lot. Knowing that it can affect you later in life would make you want to not impulsively do something. Visualizing that you will have money growth in certain aspects of life you do right will make you want to keep doing financial things right.

There are steps you can take to better yourself to have the mindset to be patient and not have that impulse. If you are practicing being patient and not having that impulse you can track your progress. All the patience and skills for finances you can teach a young child, so, when they get older they know how to wait for long-term success. Then later show them that it will help them to be able to save up their money.

The big part of delayed gratification that will make you successful in your financial part of life is being patient, not having your emotions beat the want of having your long-term goal. Think about why you are not wanting short-term pleasure. Know that the long-term goal is worth the wait, and you can have more money to save up for the actual house or car you’ve been wanting.

Amazing, beautiul, creative, and everything we need in this world!! ❤

LikeLike